What can you do with gold?

Open an Aufort gold account, and you will enjoy all of the following benefits.

Open an Aufort gold account, and you will enjoy all of the following benefits.

Bank transfers can be time-consuming and costly.

Send gold next door or to the other side of the world. It’s fast, secure, and free.

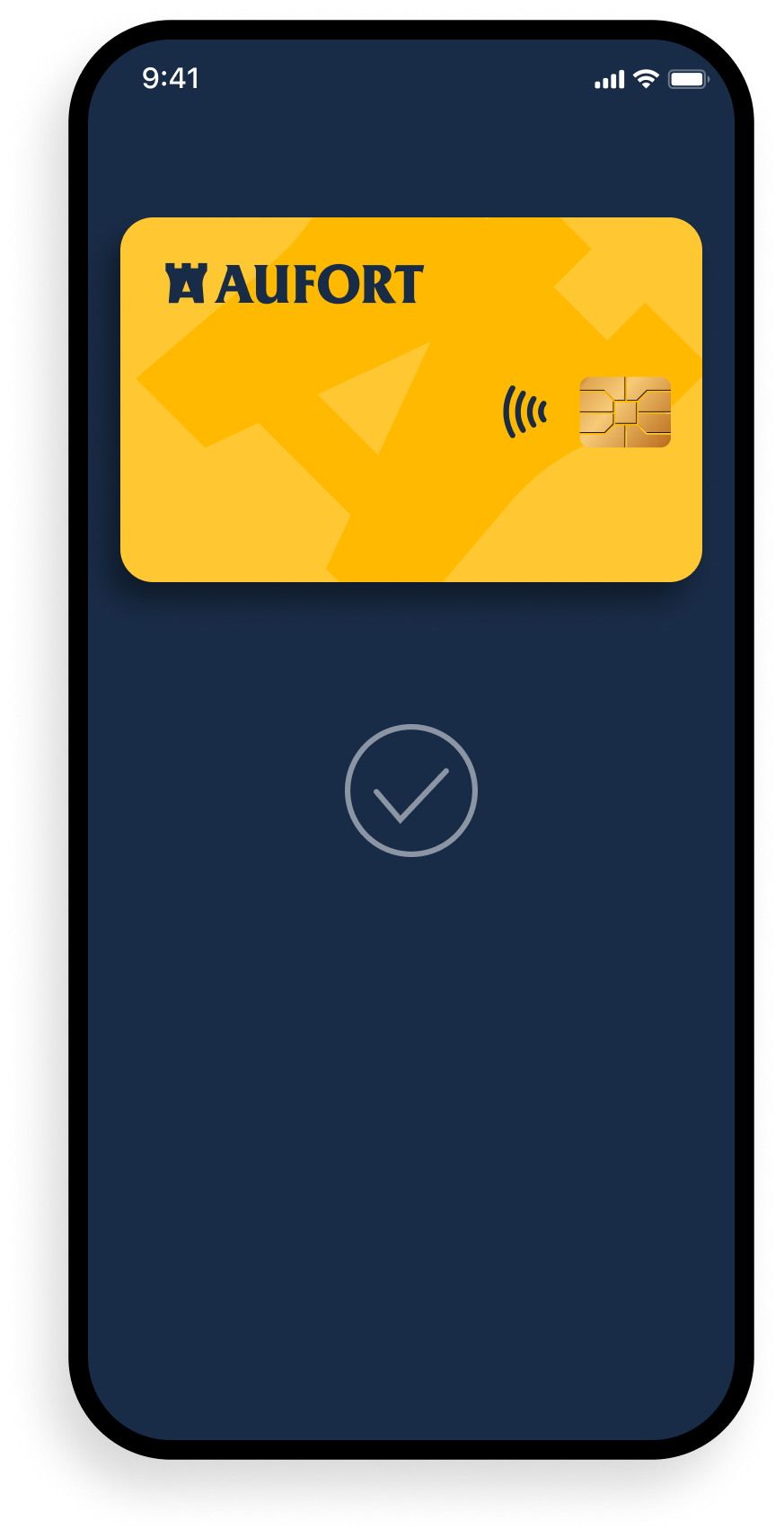

We are developing a solution that allows you to use gold as a payment method – similar to a bank card or Apple Pay, for example.

The payment service will be provided by a licensed third party.

Leave your details and when the solution is ready, you will be the first to know.

Leave detailsAufort operates in accordance with the legislation of the Republic of Estonia and the European Union, as well as international AML and KYC regulations.

We have been awarded E-commerce Trustmarks in Estonia and Europe.

Your gold is stored with our partners’ secure and audited vaults, where it is protected by insurance.

To ensure the security of your gold account, we enable activation of Google Authenticator 2-Step Verification.

We use transparent distributed ledger technology to verify the existence and ownership of gold.

Our reliable and fraud-minimizing personal identification solution is based on artificial intelligence.

Media coverage

Because your convenience is at the heart of Aufort’s innovative gold account solution.

All information concerning gold account is available even without registering as a customer.

We do not waste your time. It only takes a few minutes to register at Aufort.

We use an e-commerce platform, without any time-consuming deposits. Perform transactions immediately after registration.

All you need is the recipient’s email address, and the gold will reach them in seconds.

There are no direct or hidden fees for sending gold. It’s completely free for you.